Process owners, process steward, process custodians—many words you may have heard thrown around over the past few years. As the concept of process ownership is slowly getting traction across the board, organisations are appointing process owners more frequently than ever, and process ownership is starting to get included in role descriptions.

Why is that? Why do you even need someone to manage a process when it is intrinsically the objective of a company to perform as best it can? Because each individual trying their best to make a company succeed is not sufficient anymore: there is a clear need to layout, measure, and improve processes systematically—and, for that, someone needs to be responsible for those processes.

A wide array of definitions

Let’s start with the necessary step of defining process ownership. Perusing the interwebs provides many definitions of the concept, some with important differences. Let’s take, as a starting point, 6 sigma’s definition, the broadest one identified: “Process owners are responsible for the management of processes within the organisation.”[1]

Process Owners (POs) are responsible to manage processes. What does manage mean? This definition does not say.

Then follows two definitions with conflicting elements, illustrating well the potentially confusing nature of the process owner. On the one hand, the business dictionary defines it as “[a] person who has the ultimate responsibility for the performance of a process in realising its objectives measured by key process indicators, and has the authority and ability to make necessary changes.”[2] On the other hand, we, at Leonardo, think of the role as more of a facilitator, where the process owner is accountable for responding when process performance is outside of the accepted range (or trending in that direction), and when a change of target is appropriate. A seemingly small difference at first, it is a crucial matter when it comes to practical applicability.

Toothless tigers?

As my colleague Roger Tregear wrote in his paper Thoughts on the Conflicted Use of Process Language,[3] “differences in the definition of basic concepts in and around BPM are not just of pedantic or pedagogic interest, they cause a lot of wasted time and create confusion, which handicaps development”. There is a fundamental difference between having ultimate responsibility for a process, and being accountable to respond when your process does not perform as expected.

It boils down to the following: for a PO to be responsible for the performance of the process, he/she would need to:

- be responsible for the performance of something over which they don’t have complete control of (i.e. in the case of cross-functional processes, one specific person would be responsible for the performance across departments);

- have ultimate design authority (e.g. change whatever they like), which can be impractical and conceptually hard to sustain at lower levels.

Most companies are not ready to let their POs have such power within the organisation. This is why many choose to define the role as an addition to influence (in this way becoming less of a process owner, but more of a process custodian or steward), not an additional responsibility managers need to be worried about. But such POs can be perceived as ‘toothless tigers’, unable to truly effect change—which is why some organisations can give full responsibility and accountability for process performance to their process owners, the tooth-y tigers, if you will.

‘Owning’ processes in financial institutions

With banks expecting more mergers and acquisitions around the world, and in Australia,[4] we are starting to see the emergence of many organisations with standardised processes under the leadership of a single-point owner. One of the keys to such an operating model is having process ownership for end-to-end global standard processes, with variations only determined by tax and legal requirements.

Combined with mergers and acquisitions, technological changes have been an important driver of change in Australian banking. The different software solutions used to manage any bank are already being pressured for more agility and reduced costs. However, with an expectation for financial institutions to always deliver more to their clients (in the form of phone apps, and online credit cards or loan applications) legacy systems may have to be radically transformed to provide the expected customer experience. We are not talking about just reducing the cycle time of an application to X weeks, we are talking about reducing it to X clicks. Another big change in the Australian banking technology landscape is, at the time of this writing, the upcoming release of the New Payments Platform (NPP), which is due in the second half of 2017. The new infrastructure will provide Australian businesses and consumers with a fast, versatile, data-rich payments system for making their everyday payments. Payments will be made quickly between financial institutions and their customers’ accounts. The system will enable funds to be accessible almost as soon as payment is received—even when the payer and payee have accounts at different financial institutions.[5] Managing processes just became more complex!

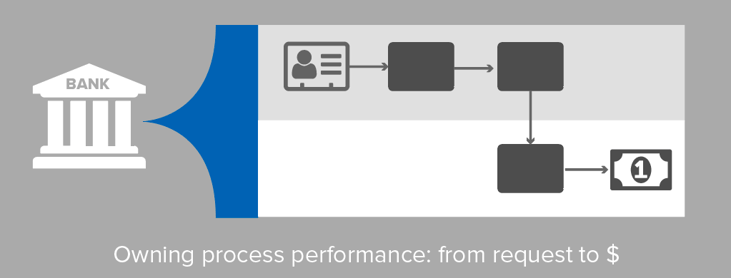

This is why the process ownership concept is becoming very important, as many of main processes of financial institutions are inherently cross-functional. Let’s look at one of the main revenue source for a bank: loans. Loans (be they commercial, personal, home mortgage, or even a small credit card advance) involve all, or almost all, of the organisation. The creation of a new loan type is a strategic decision made with the analysis of the finance department; the promotion of that product is done by marketing, while operations would process applications—and so on. Loans, though, are just one example, as many other core financial sector processes could benefit from process owners: transactions (deposits, withdrawals), financial advisory, foreign exchange, or investments (trading, superannuation).

The separate contributions of those various departments to eventually provide a loan to a customer requires cross-functional oversight. Why? Because localised (meaning inner silo) management and improvement could be done at the expense of the global loans process: marketing will be driven by sales; operations might be driven by cycle time to fulfil a loan request needed to deliver; while finance would aim at cost reductions. To orchestrate such complex process, a process owner is required.

This is becoming more crucial as banking regulators take a lot more interest in end-to-end process views: with different business lines, departments, countries, etc. Providing the right level of transparency to comply with regulations has been getting harder, but managing the risks (and related controls) of such processes has become increasingly complex.

‘Owners’ of intangible processes

It is particularly important, and beneficial, for the financial sector to appoint process owners, as the sector is quite prone (due to a lot of immaterial/intellectual work) to outsource people and non-strategic processes (reconciliation, basic accounting) in functional areas to drive costs lower. This can go beyond the sole operating structure that banks now must manage on top of their subsidiaries. Some products can be designed at the ‘main’ company, but are then packaged and sold through a subsidiary. Who then owns that process? Who ensures that it runs smoothly? Someone needs to be responsible to ensure all the connection points—between departments, physical locations, etc.—are looked after. Through process ownership, appointed key individuals (often C-level executives) are held accountable for building, standardising, and maintaining processes throughout that business’ operating structure.

So how do you make process ownership happen? This is no trivial task, but it does not have to be complex. Here are some tips to make PO happen at high level in banks and other financial institutions:

- Establish an infrastructure to ensure top-down support—with an executive sponsor, a cross-functional steering committee, and process owners.

- Start by appointing process owners for the first two or three levels of your process architecture, so they can manage the process and respond to the process’ KPIs. You can (and probably should) start small, but always top-down.

- After a few cycles and readjustments, propagate the concept to lower levels of the organisation as required. We found that meetings of process owners contributing to same value chain from different departments to be very useful in making process ownership pervasive in any organisation.

Conclusion

Banks are now primed more than ever to undergo a global transformation of governance infrastructure to align processes, people, and technology. They can enable optimisation by eliminating ineffective methods across their business units’ operating models.

With processes—and their governance through process owners—banks and other financial organisations can manage critical processes across departments, service centres, entities, or physical locations—ensuring connections points, and overall performance, are managed and improved.

[1] https://www.isixsigma.com/implementation/change-management-implementation/process-ownership-vital-role-six-sigma-success/

[2] http://www.businessdictionary.com/definition/process-owner.html

[3] http://blog.leonardo.com.au/thoughts-on-the-conflicted-use-of-process-language

[4] https://www2.deloitte.com/au/en/pages/financial-services/articles/financial-services-ma-predictions-2017.html

[5] http://www.apca.com.au/about-payments/future-of-payments/new-payments-platform-phases-1-2